Understanding Closing Costs in California: A Simple Guide for Buyers and Sellers

Buying or selling a home involves more than just agreeing on a purchase price. There are several services required to safely transfer ownership of a property, including escrow services, title insurance, recording fees, and taxes.

These expenses are commonly referred to as closing costs. In California, certain costs are typically paid by the buyer and others by the seller, although everything can be negotiated as part of the purchase agreement.

This guide explains the most common closing costs and how they are typically divided between buyers and sellers.

What Are Closing Costs?

Closing costs are the fees associated with completing a real estate transaction. These costs cover services such as:

Escrow administration

Title insurance

Recording documents with the county

Transfer taxes

Loan-related fees

Both buyers and sellers usually have closing costs, but the types of expenses differ depending on each party’s role in the transaction.

Common Closing Costs for Sellers

Sellers typically pay the costs associated with transferring ownership of the property.

Typical seller closing costs may include:

Real estate commissions

Owner’s title insurance policy

County transfer taxes

Escrow fees (often split with the buyer)

Mortgage payoff balance

HOA document or transfer fees

Disclosure reports such as Natural Hazard Reports

Property tax prorations

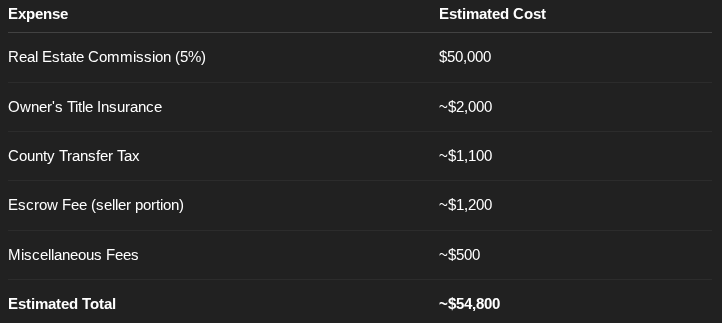

Example Seller Closing Costs

Example based on a $1,000,000 home sale:

Actual costs vary depending on the property, escrow company, and negotiated terms of the contract.

Common Closing Costs for Buyers

Buyers typically pay the costs associated with obtaining financing and setting up the new mortgage.

Typical buyer closing costs may include:

Loan origination fees

Lender underwriting fees

Appraisal

Credit report

Lender’s title insurance policy

Escrow fees (often split with seller)

Recording fees for the new loan

Home inspections

Homeowners insurance

Prepaid property taxes and interest

Example Buyer Closing Costs

Example based on a financed purchase:

These estimates vary depending on the purchase price, loan program, and lender requirements.

What Does Escrow Do?

Escrow is a neutral third party that manages the transaction and ensures that all conditions of the purchase agreement are met before the sale closes.

The escrow company typically:

Holds the buyer’s deposit

Coordinates documents between parties

Pays off existing mortgages

Collects and distributes funds

Records the new deed with the county

Escrow protects both the buyer and seller by ensuring that no funds or property transfer until all terms are satisfied.

What Is Title Insurance?

Title insurance protects homeowners and lenders from potential legal claims against the property related to past ownership.

Examples of issues title insurance may protect against include:

Unpaid liens

Errors in public records

Unknown heirs claiming ownership

Forgery or fraud in past documents

There are two common types of policies:

Owner’s Policy

Protects the buyer’s ownership rights.

Lender’s Policy

Protects the mortgage lender’s financial interest in the property.

Are Closing Costs Negotiable?

Yes. While there are customary practices in California, closing costs are ultimately determined by the purchase agreement negotiated between the buyer and seller.

For example, a seller may agree to credit the buyer for some closing costs to help complete the transaction.

Your real estate professional and escrow officer will provide a final settlement statement before closing that clearly outlines all costs involved.

Final Thoughts

Understanding closing costs early in the home buying or selling process helps prevent surprises at closing. While every transaction is unique, knowing what costs are typical can make the process much smoother.

If you have questions about closing costs, financing options, or the escrow process, feel free to reach out anytime.